By Erin Caddell, Anchor Advisors, in partnership with GK Strategy

A recently announced Trump Administration plan for the U.S. maritime industry is likely to open new opportunities for U.S.-focussed companies, investors, training businesses and even real-estate developers interested in reigniting the domestic shipbuilding industry and its related value chain – while presenting commensurate challenges in invigorating an industry that has been forsaken in favor of foreign competitors for decades.

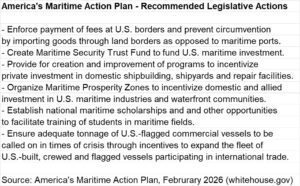

Entitled “America’s Maritime Action Plan”, the proposal released last month responds to a long-held but still shocking fact: that despite boasting the world’s largest economy, a long history of engineering and technological innovation at sea, and over 150,000 kilometers (95,000 miles) of shoreline, less than 1% of the world’s ships are built in the U.S.

It was not always so. U.S. shipbuilding was key to Allied success in both world wars. The U.S. remained the world’s largest shipbuilder as late as 1975, according to the U.S. Trade Representative. The decline of domestic shipbuilding echoes that of many American manufacturing sectors in the post-World War II era, with foreign countries using cost advantages in labor and materials to siphon away an industry once dominated by American companies. Today, 74% of the world’s commercial ships, 80% of ship-to-shore cranes and 96% of shipping containers are built in China, according to the White House. U.S. reliance on foreign shipping presents a national-security risk commonly cited by Republicans and Democrats as rivalry between China and the U.S. has intensified.

The Maritime Action Plan was set in motion by an executive order signed by President Trump in April 2025 and attempts to address this imbalance. It focuses on four pillars: 1) Rebuild domestic shipbuilding capacity; 2) Reform maritime workforce education and training; 3) Protect the maritime industrial base; and 4) Enhance national security, industrial security, and industrial resilience.

The Action Plan also recommends establishing Maritime Prosperity Zones (MPZs) would be modeled on the Opportunity Zones (OpZones) included in the Tax Cuts and Jobs Act (TCJA), the tax bill passed by Trump Administration and the Republican-controlled Congress in 2017. OpZones are census tracts designated as economically distressed areas where investors can receive tax benefits for long-term investments. OpZones were made permanent and the tax incentives expanded further in federal legislation passed in July 2025. The Action Plan recommends establishing 100 MPZs, ensuring these areas are geographically diverse and include regions outside traditional coastal shipbuilding centers.

What does this mean for companies and investors? Like many government white papers, the Maritime Action Plan is loaded with recommendations and big ideas, many of which are unlikely to become reality. And the plan acknowledges that a number of its initiatives would require Congressional legislation (see below), many with funding required – not an easy task given partisan rancor in Washington, D.C, and high U.S. budget deficits. Nonetheless, the plan touches a nerve as both U.S. political parties have grown more concerned in recent years about reliance on China in a number of industries from pharmaceuticals to rare earths to solar panels. We do see the Trump Administration continuing its focus on domestic shipbuilding given its focus on reshoring American manufacturing activity and reducing dependence on foreign partners for critical infrastructure. Democrats would likely support many of the work streams outlined in the Action Plan as well, especially as the investments outlined would help both red and blue states (many U.S. shipyards are heavily staffed by union workers, a traditional Democrat constituency). A contact who attended a recent annual U.S. shipbuilding conference reported that attendance was double or more the year before, with discussions dominated by the Administration’s new maritime strategy.

Revitalizing the domestic shipbuilding industry and its related labor and supply chains will take years. But in the interim, other opportunities may well present themselves to maritime operators and their owners: domestically made and operated software to track ships; the aforementioned Maritime Prosperity Zones; and revitalized maritime education and training programs, just to name a few. In a fractious Washington – one in which control of the seas have come rapidly to the fore again through the recently U.S.-initiated conflict in the Gulf – the U.S. domestic maritime industry may well set sail.

Want to learn more? Reach out to GK’s U.S. partner Erin Caddell at e.caddell@anchor-advisors.net.